A few days ago, there are two things that happened to Apple, which are worth pondering.

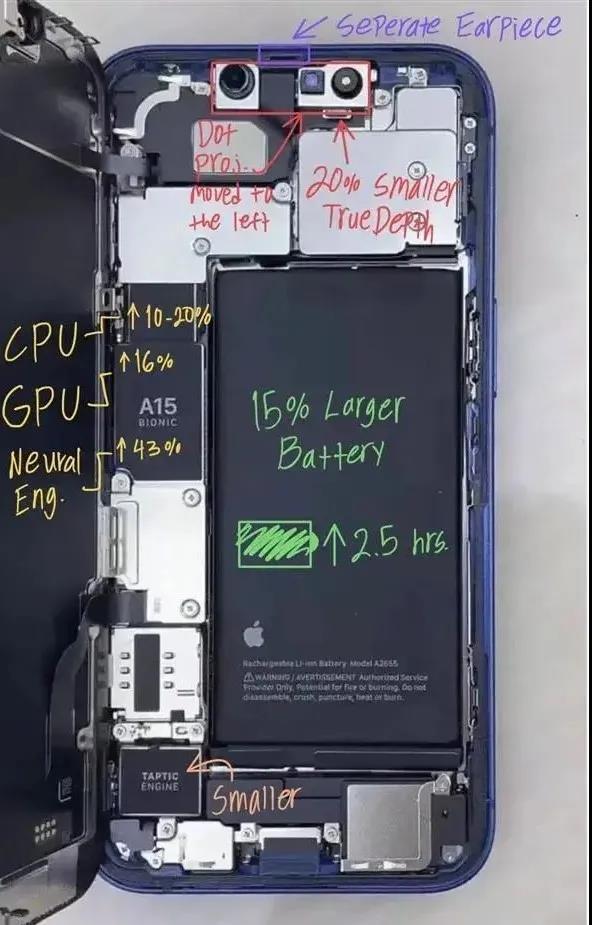

One is that a dismantling of parts and components for the iPhone 13, which has sparked heated discussions in the industry.

From the disassembly, it is found that the baseband of the iPhone 13pro comes from Qualcomm, the CPU/GPU is self-developed by Apple, and the power IC chip is supplied by Apple itself. The screen and memory are from Samsung, the flash memory is from Japan’s Toshiba (Kioxia), and the CMOS sensor is from Japan’s Sony. The core SOC of the WIFI6 module comes from Broadcom’s BCM4387. These core components account for 70% of the entire BOM cost.

Of course, there are also many parts from domestic suppliers, including lenses, batteries, housings, plates, wires, PCB boards, motors, antennas, microphones, speakers, etc. For example, BOE provides mobile phone control panels, Lens Technology produces mobile phone metal casings, and Sunny Optical provides mobile phone lenses.

In other words, in the iPhone13 series products, none of the core components are from Chinese suppliers, and Apple has relatively achieved independent control of its core components and reduced its dependence on China’s supply chain. In the dismantling report, the iPhone 13 actually revealed the big but not strong part of the domestic Apple supplier.

In addition, a noteworthy signal is that Apple eliminated 34 Chinese suppliers, including OFILM. In other words, on the one hand, Apple is reducing the proportion of Chinese suppliers, on the other hand, it has strengthened its control of core components and continued to weaken the core position of Chinese suppliers in the entire Apple supply chain.

The reason why Apple is consciously weakening the core position of Chinese suppliers in Apple’s supply chain is because China has always accounted for more than half of Apple’s supplier list.

The components in the new iPhone13 series released this year come from more than 200 suppliers, and China still accounts for more than 110 of them.

For companies in these non-core areas, Apple is also continuing to maintain its dominance and control over these non-core components through the dual-supplier model. All non-core components are basically shared by two or more companies. Supply allows these companies to compete with each other and reduce costs. If necessary, one of them can be eliminated and new manufacturers can be cultivated to join.

Apple is trying its best to prevent any company from threatening Apple’s control of this component, and it also allows most non-core component supply chain manufacturers to have no right to speak.

Even so, Apple under Cook’s rule is still not at ease. Judging from recent trends, it has been trying to expand production capacity and factories in India and Vietnam, expand the list of supply chain manufacturers, and spread the supply chain as far as possible in different countries around the world. It relies too much on the problems of suppliers in the Chinese market and strengthens its dominance.

However, at least for the time being, although none of the Chinese suppliers have entered Apple’s key core component manufacturers for products such as the iPhone, they are still focusing on camera modules, PCB circuit boards, antennas, FPC flexible printed circuit boards, and speakers. For touch motors, glass covers, glass back covers, metal structural parts, precision connectors and other non-core parts, Apple still has difficulty finding a perfect replacement outside the Chinese market.

Because these components are involved, only the Chinese market has a complete supply chain system.

For example, from the perspective of a typical enterprise-

BOE provided the control panel of the mobile phone, Lens Technology produced the metal casing of the mobile phone, Goertek provided the acoustic module for the iPhone; Taijun Technology provided the flexible PCB board, Desai battery and Xinwangda provided the mobile phone battery, ASE Kunshan The company provides substrate materials, packaging and testing services; Global Wafer Kunshan Plant and Pegatron do wafer foundry, and Lens Technology and Bourne Optics provide Apple with glass cover plates. Zhejiang Crystal Optoelectronics provides IRCF, Jinlong Electromechanical provides linear motors for iPhone, USI provides WiFi modules, Luxshare Precision supplies data cables, AAC Technologies supplies audio equipment, Sunny Optical produces lenses, Luxshare Precision, Yingtong Communications, Many domestic suppliers such as Dongshan Precision provide wireless charging coil modules and so on.

These parts produced by domestic companies do not involve key core technologies, and they can be replaced if there is a problem or the quality is not good enough. But in general, Apple wants to replace these companies, but only in the country. In foreign countries, whether it is Vietnam or India, it is still difficult to ensure that it meets the product quality and standards of Chinese factories.

Because in China, various accessories are provided around the production of iPhone, including antennas, frames, coatings, films, and various modules. These components are currently produced by enterprises in Guangdong, Fujian, and Shanghai, whether it is India or Vietnam. , Thailand and other countries are unable to produce high-efficiency supply in the first time, and even the yield rate cannot be guaranteed.

Secondly, in China, entities such as Huaqiangbei, Zhongguancun, and South China City, as well as the network electronic parts market, can quickly purchase all the materials for the production of a product and deliver them to the factory.

According to previous statistics, it takes about 400 processes to assemble an iPhone, including polishing, welding, drilling and screwing. It can produce 500,000 iPhones in a day, which is roughly equivalent to 350 in one minute. This is difficult to do in other countries and regions. It is related to iPhone production, shipping efficiency, and product quality control and quality.

This is why many of Apple’s suppliers in China have been affected by the power restriction and have affected the normal shipment of the iPhone 13 series of mobile phones. The iPhone 13 series therefore ushered in the longest waiting period.

Behind this, on the one hand, because of the advancement of domestic manufacturing technology, the manufacturing industry has a relatively complete supply chain system and channel system and the electronic retail market, on the other hand, China has a large number of skilled and relatively cheap industrial workers.

For example, China’s foundries contribute most of the assembly and production business for the iPhone. The factories in China account for over 60% of Foxconn’s production capacity. Luxshare Precision has also risen. The OEM’s production business is the most critical and core. Resources are skilled industrial workers.

A large number of skilled industrial workers has brought better electronic material processing technology, deposition and coating technology, complex testing and assembly capabilities to the Apple iPhone. These capabilities are the manufacturing field in which China’s skilled industrial workers dominate, and they are also the iPhone series. Product production and processing and product quality have brought better help.

Therefore, we can conclude that, from the perspective of core technology, the Chinese supply chain surrounding Apple presents the characteristics of being large but not strong. But despite this, China’s national chain suppliers still have irreplaceable value for a certain period of time, and Apple cannot replace them all in the world.

But in general, Apple is still trying to expand the list of suppliers. Data shows that Apple under Cook’s rule has increased the number of suppliers from about 150 in the Jobs era to 800. The expansion of suppliers has also relatively diluted China. Percentage of suppliers.

Basically, Apple no longer has to worry about being controlled by a certain company in the supply chain. In addition, Foxconn is also expanding overseas production capacity and said that overseas foundry production capacity has increased to 30%.

Apple’s grand strategy is to reduce its dependence on Chinese suppliers. Under this strategy, domestic supply chain companies are also in crisis and uncertainty. For example, relying on Apple’s orders, its lens module supply chain is Ranked No. 1 in the world, but after being kicked out of the supply chain by Apple, OFILM’s profit plummeted 90%.

This is actually an early warning for Chinese fruit chain suppliers. iPhone13 reveals a corner of the domestic Apple supply chain that is large but not strong. How to gain living space and strengthen competitiveness in the future is worth considering for these manufacturers.

In the author’s opinion, there are many ideas. The first is to make up for the shortcomings and overcome the core key technical areas. If this shortcoming is not made up, then the domestic supply chain’s position in the middle and lower reaches of the industry will never be changed. This is A difficult but necessary breakthrough.

The second is to put eggs in multiple baskets to reduce dependence on Apple’s business. On the one hand, you can cooperate with Apple, but you can’t put all your energy and profit on it. Apple is good at putting eggs in multiple baskets. There are two or three alternatives, and Chinese supply chain companies should do the same. At the level of building parts, they should focus part of their energy on other manufacturers such as domestic mobile phones.

For example, some companies have deployed multiple manufacturers. The domestic mobile phone panel manufacturer Lens Technology has begun to actively cooperate with domestic mobile phone brands. Now Huawei has become the largest user of Lens Technology. In this way, even if one day is Abandoning the apple will not make it impossible to survive.

Of course, this will also become a trend, because if domestic suppliers cannot share the high profits of the Apple ecosystem and are in a crisis of being abandoned at any time, they will naturally turn to serve other growth momentum and stability. Vendors with better certainty. Manufacturers in the supply chain that can meet Apple’s needs naturally have certain experience to promote the demand and capacity upgrades of domestic manufacturers, and it is relatively compatible with the needs of domestic mobile phone manufacturers.

The second is to diversify the development of customers, expand new business space in the upstream and downstream directions such as notebooks, PCs, and VRs, and at the same time invest as much research and development as possible to improve technology and product quality, and achieve irreplaceable value.

In addition, a question worth considering is the future of manufacturing.

We know that the core advantage of China’s manufacturing industry lies in the relative integrity of China’s entire manufacturing industry chain and the presence of a group of skilled industrial workers. These skilled industrial workers have irreplaceable value in the world.

However, judging from the current manufacturing situation, the industry’s attractiveness to young people is decreasing, and many young people are becoming less and less willing to enter the manufacturing sector. Correspondingly, there are more and more young people delivering food. , This is a big worry about whether the domestic manufacturing advantage can be maintained in the future.

The domestic manufacturing industry is not like the developed countries in Europe and the United States, which naturally develops to the top after the natural expansion of globalization, but when the industrial foundation and technological level of the manufacturing industry are still in the development stage, capital, labor and talents are far away from manufacturing. The industry, which flows to real estate, Internet, finance and other fields where money is fast, lacks a real awe and attention to the real economy and manufacturing industry.

For the domestic manufacturing industry, it is undoubtedly very difficult to not only be able to upgrade the industry, but also to retain industrial workers. How to form core advantages and migrate upstream before the division of labor in the global manufacturing industry is also a difficult problem that the domestic manufacturing industry needs to think about.

Apple’s approach has also given manufacturers a wake-up call, how to maintain their manufacturing advantages and how to ensure that the core value and destiny of supply chain manufacturers are in their own hands. There is only one answer, which is to do it in their own core hinterland. To be irreplaceable and always have Plan B.